CashNews.co

Despite recent turbulence in global markets, Japan’s stock indices have shown resilience, with the Nikkei 225 and TOPIX Index experiencing notable fluctuations. This backdrop of economic shifts and investor sentiment offers a unique opportunity to explore lesser-known small-cap stocks that could offer potential growth. In this context, identifying a good stock often involves looking for companies with strong fundamentals, innovative products or services, and the ability to navigate economic uncertainties effectively. Here are three undiscovered gems in Japan that exemplify these qualities for September 2024.

Top 10 Undiscovered Gems With Strong Fundamentals In Japan

|

Name |

Debt To Equity |

Revenue Growth |

Earnings Growth |

Health Rating |

|---|---|---|---|---|

|

Ryoyu Systems |

THAT |

1.08% |

8.08% |

★★★★★★ |

|

Central Forest Group |

THAT |

7.05% |

14.29% |

★★★★★★ |

|

Poppins |

39.80% |

8.36% |

-7.40% |

★★★★★★ |

|

Kanda HoldingsLtd |

30.47% |

4.35% |

18.02% |

★★★★★★ |

|

NJS |

THAT |

4.97% |

5.30% |

★★★★★★ |

|

Ad-Sol Nissin |

THAT |

4.02% |

7.90% |

★★★★★★ |

|

NPR-Riken |

15.31% |

10.00% |

44.55% |

★★★★★☆ |

|

That one |

82.16% |

1.83% |

47.38% |

★★★★★☆ |

|

AJIS |

0.69% |

0.07% |

-12.44% |

★★★★★☆ |

|

Pharma Foods International |

191.14% |

33.83% |

23.46% |

★★★★★☆ |

Click here to see the full list of 749 stocks from our Japanese Undiscovered Gems With Strong Fundamentals screener.

We’ll examine a selection from our screener results.

Simply Wall St Value Rating: ★★★★★★

Overview: G-Tekt Corporation manufactures and sells auto body components and transmission parts in Japan and internationally, with a market cap of ¥68.67 billion.

Operations: G-Tekt generates revenue primarily from the sale of auto body components and transmission parts. The company operates with a market cap of ¥68.67 billion.

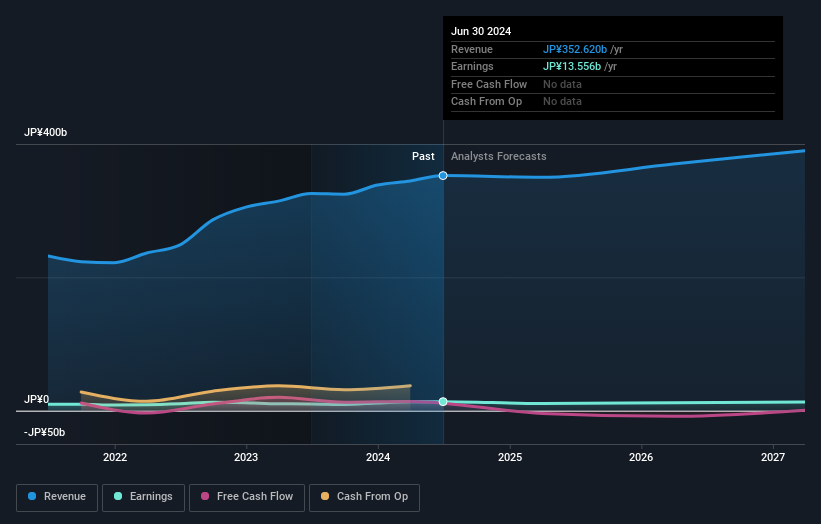

G-Tekt, a small cap player in the auto components industry, has shown impressive performance with earnings growth of 33.5% over the past year, outpacing the industry’s 21.4%. The company’s price-to-earnings ratio stands at 5.1x, significantly lower than Japan’s market average of 13.2x, indicating good value relative to peers. Additionally, G-Tekt’s debt-to-equity ratio improved from 34.1% to 18.5% over five years and remains free cash flow positive.

Simply Wall St Value Rating: ★★★★★★

Overview: Kamei Corporation operates as a general trading company in Japan and internationally with a market cap of ¥66.09 billion.

Operations: The primary revenue streams for Kamei Corporation are the Energy Business (¥279.16 billion) and Overseas/Trade Business (¥84.52 billion), followed by the Automotive Related Business (¥75.41 billion). The Food Business also contributes significantly with ¥36.47 billion in revenue.

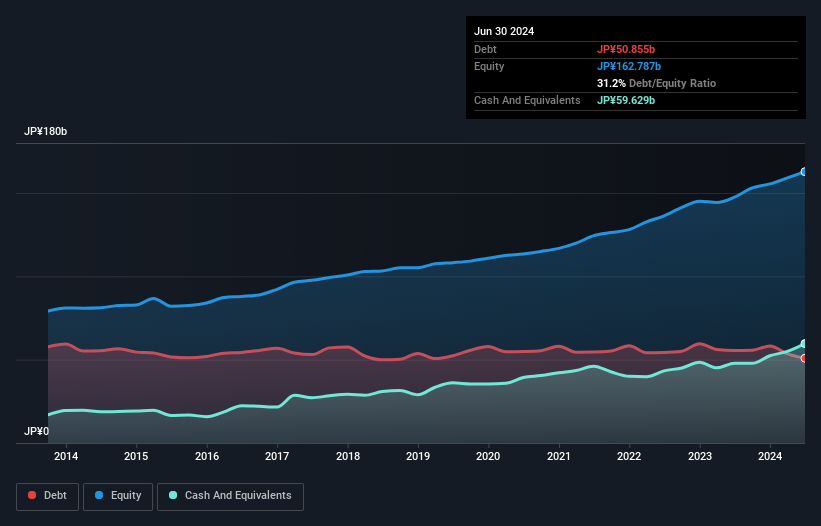

Kamei, a small cap in Japan, has been trading at 69.7% below its estimated fair value. Over the past year, earnings grew by 11.1%, outpacing the Trade Distributors industry growth of 6.7%. The company repurchased 800,000 shares for ¥1.45 billion between May and June this year, representing 2.38% of outstanding shares. With high-quality earnings and positive free cash flow, Kamei’s debt to equity ratio improved from 48.4% to 31.2% over five years.

Simply Wall St Value Rating: ★★★★★☆

Overview: Marusan Securities Co., Ltd. operates in the financial products trading sector in Japan with a market cap of ¥64.08 billion.

Operations: Marusan Securities Co., Ltd. generates revenue primarily from trading financial products in Japan. The company has a market capitalization of ¥64.08 billion.

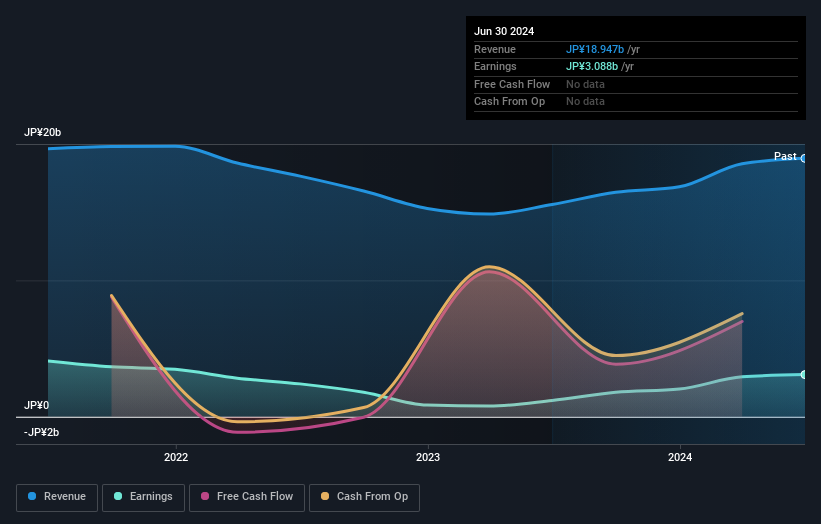

Marusan Securities, a smaller player in Japan’s financial sector, has shown remarkable earnings growth of 158.6% over the past year, outpacing the industry average of 36.1%. The company’s debt to equity ratio improved from 6.6 to 5.3 over five years, indicating better financial health. With levered free cash flow reaching ¥3.85 billion as of September 2024 and high-quality earnings reported consistently, Marusan appears well-positioned for continued stability and potential growth in its niche market segment.

Key Takeaways

Want To Explore Some Alternatives?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include TSE:5970 TSE:8037 and TSE:8613.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]